-

Table of Contents

“Unlocking the Power of Banking: Your Guide to Different Account Types”

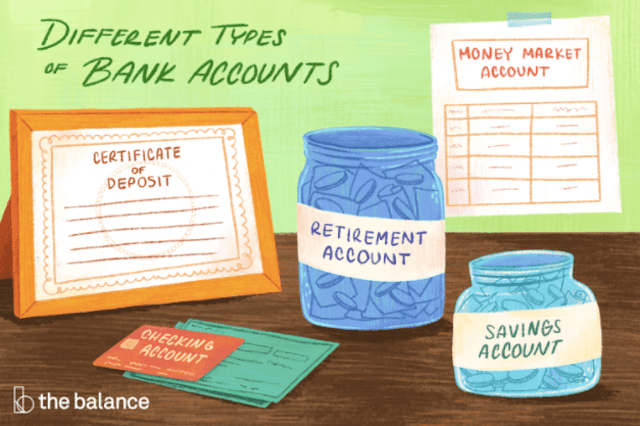

Understanding the Different Types of Bank Accounts is essential for individuals looking to manage their finances effectively. With various options available, it is important to have a clear understanding of the features and benefits of each type of account. This knowledge can help individuals make informed decisions about which account best suits their needs and financial goals. In this article, we will explore the different types of bank accounts, including checking accounts, savings accounts, money market accounts, and certificates of deposit (CDs). By understanding the unique characteristics of each account, individuals can make the most of their banking experience and achieve their financial objectives.

The Importance of Knowing the Various Types of Bank Accounts

Understanding the Different Types of Bank Accounts

When it comes to managing our finances, having a bank account is essential. It provides a safe and convenient way to store and access our money. However, not all bank accounts are created equal. There are various types of bank accounts, each with its own features and benefits. Understanding these different types is crucial for making informed decisions about our financial well-being.

One of the most common types of bank accounts is a checking account. This type of account is designed for everyday transactions, such as paying bills and making purchases. With a checking account, you can easily deposit and withdraw money, either through a physical branch or online banking. Many checking accounts also come with a debit card, which allows you to make purchases directly from your account. This type of account is ideal for those who need frequent access to their funds.

On the other hand, a savings account is specifically designed for saving money. Unlike a checking account, a savings account typically offers a higher interest rate, allowing your money to grow over time. This makes it an excellent option for setting aside funds for emergencies or long-term goals, such as buying a house or planning for retirement. While you can still withdraw money from a savings account, there are usually limitations on the number of withdrawals you can make each month.

Another type of bank account that is gaining popularity is a money market account. This type of account combines the features of both checking and savings accounts. It offers a higher interest rate than a regular savings account, while still allowing you to write checks and make withdrawals. Money market accounts are often recommended for individuals who have a larger amount of money to save and want to earn a higher return on their investment.

Certificates of deposit (CDs) are another type of bank account that can help you grow your savings. With a CD, you agree to deposit a certain amount of money for a fixed period of time, typically ranging from a few months to several years. In return, the bank offers a higher interest rate than a regular savings account. However, it’s important to note that withdrawing money from a CD before the agreed-upon term can result in penalties.

Understanding the different types of bank accounts is crucial for managing your finances effectively. By choosing the right account for your needs, you can maximize your savings and make your money work harder for you. Whether you need a checking account for everyday transactions, a savings account for long-term goals, or a money market account or CD for higher returns, there is a bank account out there that can meet your needs.

In conclusion, having a bank account is an essential part of managing our finances. However, not all bank accounts are the same. Understanding the different types of bank accounts, such as checking accounts, savings accounts, money market accounts, and CDs, is crucial for making informed decisions about our financial well-being. By choosing the right account for our needs, we can effectively manage our money and work towards our financial goals. So, take the time to explore the various types of bank accounts available and find the one that suits you best.

Exploring the Features and Benefits of Savings Accounts

Savings accounts are a popular choice for individuals looking to save money and earn interest on their deposits. These accounts offer a range of features and benefits that make them an attractive option for many people.

One of the key features of a savings account is the ability to earn interest on your deposits. Unlike a checking account, where your money typically does not earn any interest, a savings account allows you to grow your savings over time. The interest rate on savings accounts can vary depending on the bank and the type of account, but even a small amount of interest can add up over time.

Another benefit of a savings account is the ability to easily access your funds. While some savings accounts may have restrictions on the number of withdrawals you can make each month, most accounts allow you to withdraw money whenever you need it. This makes a savings account a convenient option for individuals who want to save for a specific goal, such as a vacation or a down payment on a house.

In addition to earning interest and easy access to funds, savings accounts also offer a level of security. Most banks are insured by the Federal Deposit Insurance Corporation (FDIC), which means that even if the bank fails, your deposits are protected up to $250,000 per depositor. This provides peace of mind for individuals who want to ensure the safety of their savings.

Savings accounts also come with a variety of features that can help you manage your money more effectively. Many banks offer online and mobile banking options, allowing you to easily check your balance, transfer funds, and set up automatic savings transfers. Some accounts also offer tools and resources to help you track your spending and set savings goals.

When choosing a savings account, it’s important to consider the fees and minimum balance requirements. Some accounts may charge monthly maintenance fees or require a minimum balance to avoid fees. It’s important to read the fine print and understand the terms and conditions of the account before opening it.

It’s also worth noting that there are different types of savings accounts to choose from. A basic savings account is a simple option that offers the features and benefits mentioned above. However, some banks also offer specialized savings accounts, such as high-yield savings accounts or money market accounts. These accounts may offer higher interest rates or additional features, but they may also have higher minimum balance requirements or other restrictions.

In conclusion, savings accounts are a valuable tool for individuals looking to save money and earn interest on their deposits. They offer a range of features and benefits, including the ability to earn interest, easy access to funds, security, and tools to help manage your money. When choosing a savings account, it’s important to consider the fees, minimum balance requirements, and any specialized options that may be available. By understanding the different types of savings accounts and their features, you can make an informed decision that aligns with your financial goals.

Understanding the Differences Between Checking and Money Market Accounts

Understanding the Differences Between Checking and Money Market Accounts

When it comes to managing your finances, choosing the right bank account is crucial. Two popular options are checking accounts and money market accounts. While they may seem similar at first glance, there are some key differences between the two that you should be aware of.

Let’s start with checking accounts. These are the most common type of bank account and are designed for everyday transactions. When you open a checking account, you are typically given a checkbook and a debit card, which allows you to make purchases and withdraw cash from ATMs.

One of the main advantages of a checking account is its accessibility. You can easily deposit and withdraw money whenever you need to, making it convenient for managing your day-to-day expenses. Additionally, most checking accounts offer online banking services, allowing you to monitor your transactions and pay bills electronically.

However, checking accounts usually offer very low or no interest rates. This means that the money you deposit into a checking account will not earn much, if any, interest over time. If you have a large sum of money that you don’t need immediate access to, you may want to consider a money market account instead.

Money market accounts are similar to checking accounts in that they offer easy access to your funds. However, they typically come with higher interest rates, making them a more attractive option for those looking to grow their savings. Money market accounts also often come with a minimum balance requirement, meaning you need to maintain a certain amount of money in the account to avoid fees.

Another key difference between checking and money market accounts is the level of risk involved. Checking accounts are insured by the Federal Deposit Insurance Corporation (FDIC), which means that even if the bank fails, your money is protected up to $250,000. Money market accounts, on the other hand, are not FDIC-insured. Instead, they are often invested in low-risk securities, such as government bonds, which means there is a small chance of losing your principal investment.

It’s important to note that while money market accounts offer higher interest rates than checking accounts, they still may not provide the same returns as other investment options, such as stocks or mutual funds. If you are looking to grow your wealth significantly, you may want to consider exploring other investment avenues.

In conclusion, understanding the differences between checking and money market accounts is essential for making informed financial decisions. Checking accounts are ideal for everyday transactions and offer easy accessibility, but they typically have low or no interest rates. Money market accounts, on the other hand, provide higher interest rates and are suitable for those looking to grow their savings. However, they may come with minimum balance requirements and carry a small level of risk. Ultimately, the choice between the two depends on your financial goals and needs.In conclusion, understanding the different types of bank accounts is crucial for individuals to make informed decisions about their finances. By knowing the features and benefits of various account options such as savings accounts, checking accounts, and certificates of deposit, individuals can choose the most suitable account to meet their financial goals and needs. Additionally, understanding the terms and conditions, fees, and interest rates associated with each account type can help individuals maximize their savings and minimize unnecessary costs. Overall, having a clear understanding of the different types of bank accounts empowers individuals to effectively manage their money and achieve financial stability.